A loan origination system workflow is the series of steps used to move a loan application from intake through underwriting, approval, funding, and the transfer to servicing. A clear workflow helps lenders and loan servicers reduce manual work, improve visibility, and create a more consistent process across teams.

In this guide, we’ll break down each stage of a loan origination system workflow, the challenges that slow lenders down, and best practices for building a more efficient lending operation from application to funding.

Key Takeaways

- Workflows standardize the loan process: A structured workflow moves applications through consistent stages instead of relying on ad-hoc handling.

- Manual steps create bottlenecks: Data entry errors and disconnected systems slow down approvals as loan volume grows.

- Visibility matters at every stage: Teams need clear insight into where a loan sits in the process at any given time.

- Origination connects directly to servicing: Once a loan is funded, it moves into ongoing payment tracking and portfolio monitoring.

- Configurable workflows support different loan types: Lenders managing varied portfolios benefit from rules that adapt to each loan product.

What Is a Loan Origination System Workflow?

A loan origination system workflow is a structured process that moves a loan application through defined stages, from intake to funding. It combines people, tasks, approvals, and documentation into a repeatable sequence, forming one piece of the broader loan lifecycle.

This structure creates consistency across lending operations. Instead of each loan following a different path based on who is handling it, every application moves through the same general stages:

Application → Verification → Underwriting → Approval → Closing → Funding → Servicing

That consistency is what makes a workflow useful. It gives lenders a predictable process to manage, audit, and improve over time.

Why Loan Origination Workflows Matter

Loan origination workflows matter because they reduce the manual work, confusion, and delays that come with handling loan applications inconsistently.

Manual Processes Create Delays

When data entry, document collection, and approvals are done manually, small errors and omissions slow everything down. A single missing document can stall a loan for days while staff tracks it down.

Visibility Becomes Difficult as Volume Grows

Without a defined workflow, it’s hard to know where a loan sits in the process or who is responsible for the next step. As application volume increases, this lack of visibility compounds into real operational strain.

Workflow Standardization Improves Efficiency

Defined stages and clear ownership mean fewer dropped tasks and faster movement from application to funding. A more structured loan management process gives lenders the consistency they need to identify bottlenecks and fix them, rather than guessing where time is being lost.

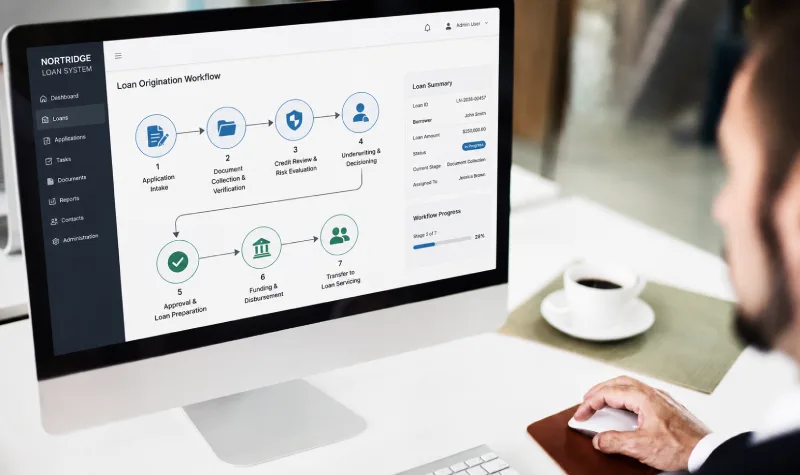

The 7 Stages of a Loan Origination System Workflow

Most loan origination workflows follow a similar loan processing workflow, though the specifics vary by lender and loan type.

1. Application Intake

The workflow begins when a borrower submits an application and the lender collects initial loan and borrower information. This stage includes data collection and an initial qualification review to confirm the application meets basic criteria before moving forward.

2. Document Collection and Verification

This stage involves gathering and confirming the documents needed to support the application, including income verification, identity verification, and other supporting paperwork. Missing document tracking helps staff identify gaps before they cause delays later in the process.

3. Credit Review and Risk Evaluation

Lenders review credit reports, risk scores, and debt levels against their internal lending criteria during this stage. This evaluation gives lenders a clearer picture of the borrower’s overall financial position before the loan moves to underwriting.

4. Underwriting and Decisioning

Underwriting involves a detailed review of the application, credit findings, and any additional conditions that need to be met. Based on this review, the loan moves toward an approval or denial decision, with more complex cases escalated for further review.

5. Approval and Loan Preparation

Once a loan is approved, internal teams finalize loan terms and prepare the documentation needed to move forward. This stage typically includes a documentation review and the creation of an audit trail to support compliance tracking later in the loan’s life.

6. Funding and Disbursement

After final checks are complete, the loan funds and disbursement begins. Lenders track disbursement details and maintain recordkeeping throughout this stage to support accurate reporting once the loan becomes active.

7. Transfer to Loan Servicing

Once a loan is funded, it becomes active and moves into servicing. Payment schedules are established, and ongoing borrower management begins, along with reporting and portfolio monitoring. This handoff marks the difference between loan origination and servicing: origination ends once funding is complete, while servicing covers everything that happens for the life of the loan.

Common Loan Origination Workflow Challenges

Lenders managing growing loan volume often run into similar operational challenges.

| Challenge | Impact |

| Manual data entry | Slower processing |

| Disconnected systems | Duplicate work |

| Missing documents | Delayed approvals |

| Limited reporting | Reduced visibility |

| Inconsistent workflows | Operational inefficiencies |

| Growing loan volume | Scalability concerns |

These challenges tend to compound. A lender dealing with disconnected systems is also more likely to struggle with reporting and visibility, since data is scattered across multiple tools instead of centralized in one place.

Best Practices for Building an Efficient Loan Origination Workflow

Lenders looking to improve their workflow can start with a few foundational changes.

Standardize Processes Across Teams

Consistent review steps and clearly defined responsibilities reduce confusion and keep loans moving through the same stages regardless of who is handling them. This also makes training new staff easier, since the process itself does not change from person to person.

Centralize Documents and Data

Keeping documentation in a single source of truth makes audits easier and reduces the time spent searching for missing files. When everything lives in one place, staff spend less time tracking down information and more time advancing loans.

Use Configurable Workflow Rules

Task routing, approval paths, and workflow triggers let lenders adapt the process to their needs rather than forcing every loan through a rigid sequence. This kind of flexible process management is especially useful for lenders handling multiple loan types with different requirements.

Improve Reporting and Visibility

Dashboards and performance monitoring give lenders pipeline visibility, helping them spot bottlenecks before they become bigger problems. Strong reporting also supports better conversations with investors and stakeholders who want insight into loan performance.

Connect Origination and Servicing Operations

A smooth handoff from origination into servicing keeps borrower data intact and avoids the disruption that comes from re-entering information into a separate system once a loan funds.

How Nortridge Supports Loan Workflow Management

Nortridge offers extensive configuration capabilities and integrates with loan origination software, giving lenders a connected system from post-funding through payoff. Once a loan moves out of origination, Nortridge supports the full borrower lifecycle with tools built for lenders managing complex, high-volume portfolios.

Nortridge’s platform includes configurable workflows, document control, audit trails, and reporting tools to support consistency and accountability. Dashboards give teams visibility into loan performance, while an extensive API framework supports integration with the other systems lenders already use.

Nortridge supports multiple loan types, helping lenders maintain a smooth transition from origination into servicing without losing data along the way.

See Nortridge in Action

Schedule a personalized walkthrough to see how Nortridge integrates with loan origination software to support a connected workflow from funding through payoff.

Frequently Asked Questions

What is a loan origination system workflow?

What are the stages of a loan origination workflow?

How can lenders improve loan origination efficiency?

What is the difference between loan origination and loan servicing?

Can loan origination workflows be configured for different loan types?

Improve Loan Workflow Visibility Across the Lending Lifecycle

An effective loan origination system workflow helps lenders reduce manual work, improve visibility, and create a more consistent borrower experience. As loan volume grows, configurable workflows, reporting tools, and centralized loan management become increasingly important for maintaining operational efficiency.

Nortridge helps lenders and loan servicers manage complex lending operations with configurable workflows, robust reporting tools, and full borrower lifecycle management.

Schedule a demo to see how Nortridge can support your team from origination through servicing.